This is the fifth post in our CSRD blog series – feel free to also check out:

- 3 major benefits of streamlined CSRD preparations

- What companies need to know about the CSRD

- Demystifying the three ‘I’s of the CSRD

- Why impact materiality is critical for double materiality assessments

- Navigating the CSRD with 7 key updates to the final ESRS Delegated Act

- Navigating recent updates to the EU sustainability agenda

More standards, more interoperability

We are experiencing a critical and exciting moment of change with the rapid evolution of sustainability reporting standards.

Increasing public reporting requirements across geographies, jurisdictions and industries create significant new workloads for companies that must now: gather data across their value chain, process information, generate relevant insights, act where change is required, and prepare public reporting – including assurance of the process in some cases.

While companies now face a veritable alphabet soup of ESG reporting standards – from the European Sustainability Reporting Standards (ESRS), to the Global Reporting Initiative (GRI), Task Force on Climate-Related Financial Disclosures (TCFD) and International Sustainability Standards Board (ISSB) – it’s important to note that there is actually a high degree of interoperability between these different standards.

In this blog, we discuss the key points companies need to know about how the EU has approached the design of the Corporate Sustainability Reporting Directive (CSRD) and which key areas of the upcoming regulation are interoperable with other standards.

The pursuit of interoperability

Almost all major sustainability reporting bodies are working diligently to deliver standards that align as much as possible with existing and emerging regulations. But to date leaders have been at pains to describe the exact degree and nature of alignment between emerging frameworks and standards.

As representatives from the EU Commission highlighted at the recent Sustainability Standards Advisory Forum in April, maximising interoperability between different sets of standards – particularly between ISSB and ESRS – is necessary to “achieve the substantive goal” of improving the quality and coherence of sustainability reporting”. (Source: Corporate Disclosures)

Standards setters therefore are pursuing interoperability as a way to provide more flexibility for companies, while also ensuring comprehensive and consistent disclosure standards globally.

CSRD as the foundational Rosetta Stone for interoperability

CSRD has established the most extensive and far-reaching sustainability reporting requirements in terms of:

- Mandatory regulation (non-voluntary disclosure)

- Geographically impactful requirements, extending even beyond the EU, and affecting up to 10,000 companies

- Double materiality included for the first time – i.e. both financial and impact materiality must be disclosed

- Data required across 82 disclosure requirements

- Scope of disclosures across the whole value chain

With this in mind, the CSRD requirements are a very strong place to start to understand not only your company’s level of readiness for forthcoming EU regulations, but also interoperability with other standards.

Interoperability by design

Under the proposed CSRD, the European Financial Reporting Advisory Group (EFRAG) was appointed as technical adviser to the European Commission for developing the European Sustainability Reporting Standards (ESRS). And in turn, EFRAG is working with the ISSB and GRI to build an interoperability mapping table.

Under the EFRAG-GRI cooperation agreement, signed in July 2021, the two organisations joined each other’s technical expert groups, committing to share information, and for standard setting activities and timelines to be aligned as much as possible.

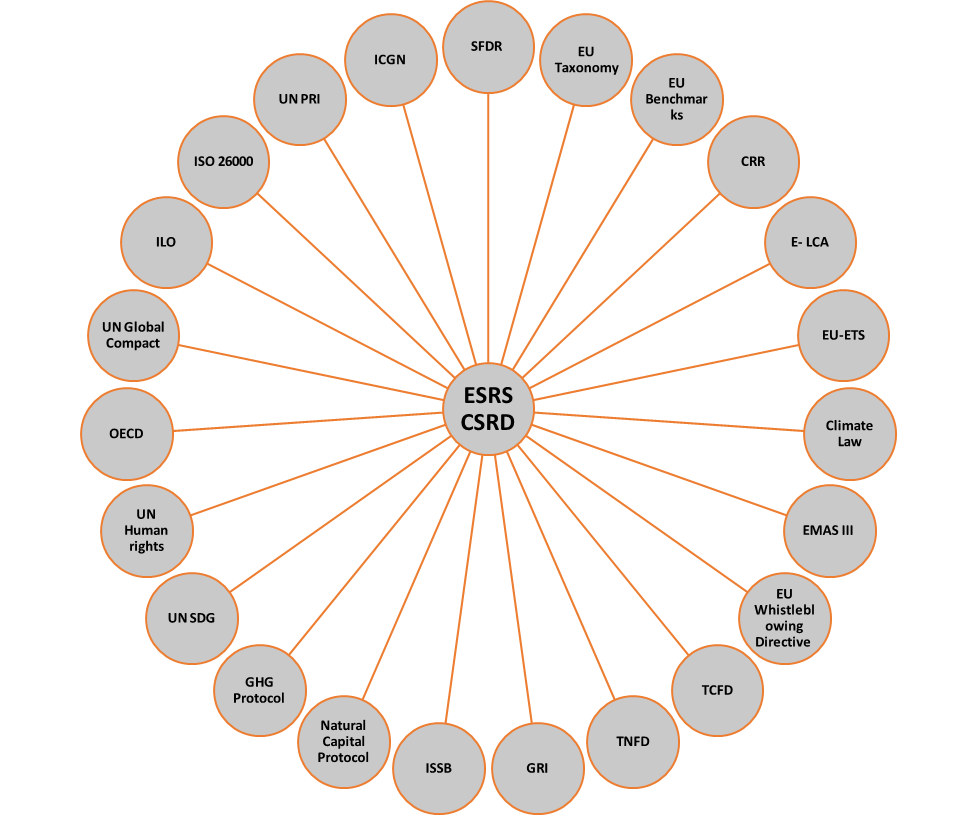

Going even further, the explanatory note of draft ESRS reflects around 23 separate initiatives, legislations and frameworks that are linked through the ESRS disclosure requirements. These include:

- Sustainability-related disclosures in the financial services sector (SFDR)

- Sustainable Finance Taxonomy

- EU Climate Transition Benchmarks and EU Paris-aligned Benchmarks

- Capital requirements regulation (CRR)

- Commission Recommendation on life cycle environmental performance of products and organisations

- EU Emissions Trading Scheme (EU-ETS)

- European Climate Law

- EU Eco-Management and Audit Scheme (EMAS) III

- EU Whistleblowing Directive

- Recommendations of the Task Force on Climate-related Financial Disclosures (TCFD)

- Recommendations of the Task Force for Nature Related Financial Disclosure (TNFD)

- Global Reporting Initiative (GRI) Standards

- Exposure Drafts (ED) IFRS S1 and IFRS S2

- Transparent Project and Natural Capital Protocol

- GHG Protocol

- UN Sustainable Development Goals

- UN Guiding Principles on Business and Human Rights

- OECD Guidelines for Multinational Enterprises

- UN Global Compact

- ILO core conventions

- ISO 26000 standard on social responsibility

- UN Principles for Responsible Investment

- ICGN Global Governance Principles

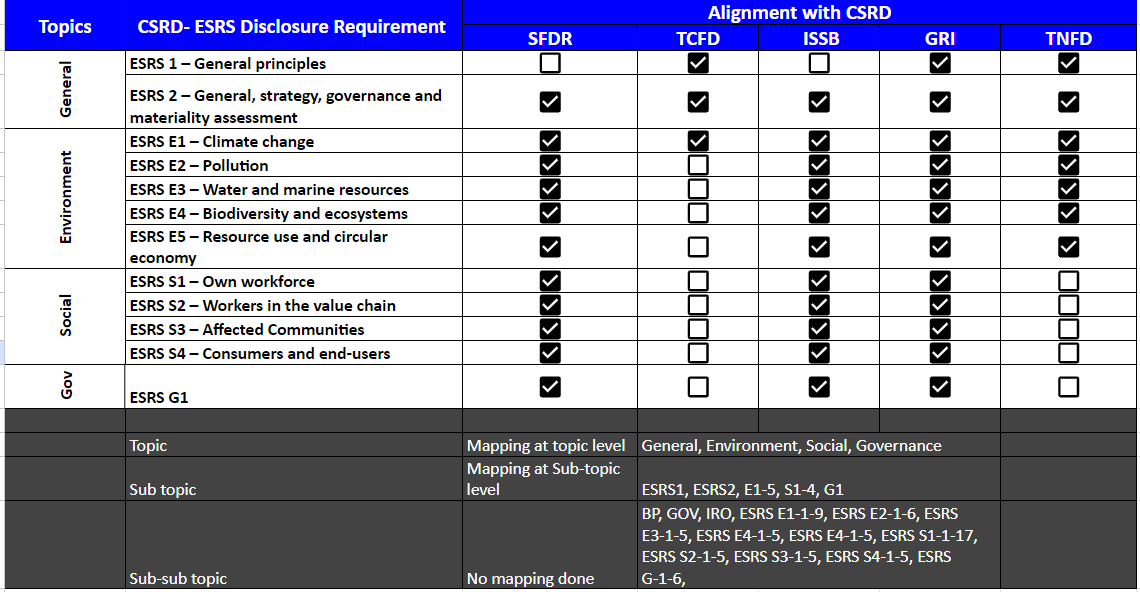

Mapping CSRD with other standards and regulations

When mapping the CSRD requirements to other standards and regulations, It’s important to first look at the hierarchy of sustainability topics in order to understand how GIST Impact has approached the following interoperability mapping exercise.

ESRS defines the sustainability matters that should be included in a company’s materiality assessment under four main categorisation levels. This includes:

(a) Level 1: TOPICAL ESRS (Environment, Social, Governance)

(b) Level 2: TOPICS (for example: Climate change, Pollution, Biodiversity, Workers in the value chain, etc.)

(c) Level 3: SUB-TOPICS (for example: Pollution of air, Water consumption, Direct impact drivers of biodiversity loss, Working conditions, etc.)

(d) Level 4: SUB-SUB-TOPICS (for example: Land-use change, Invasive alien species, Land degradation, Secure employment, Working time, Adequate wages, etc.)

Within these categories, the CSRD includes 82 disclosure requirements with approximately 1144 data points to be reported. The table below maps the interoperability of indicators at the CSRD sustainability topic level (level 2), exploring the coverage of relevant disclosure requirements with the indicators of other regulations.

As you can see in the table, any company already reporting under existing standards and/or regulatory frameworks (such as SFDR, GRI, ISSB or TCFD) is well-positioned to begin addressing the requirements under CSRD.

With numerous emerging sustainability reporting and disclosure requirements, many companies understandably struggle with where to begin. CSRD can be the ideal starting point as it is the most comprehensive legislation to date, and has robust interoperability with several other leading sustainability standards. By focusing on compliance with CSRD’s reporting requirements, companies can therefore minimise the need for additional data gathering and analysis and ensure limited room for gaps.

To discuss how GIST Impact can support you and your company with CSRD preparations, get in touch at info@18.134.187.137.