CSRD preparations march on with recent clarifications from EFRAG. Companies are now moving fast to get ready for the requirements of the EU sustainability regulations expected in 2024. GIST Impact has the data and tools to streamline preparations, and in this blog post our regulatory expert Shraddha unpicks the nitty gritty of the ‘What, How, Who and When’ In the fast-evolving world of EU sustainability, staying updated on the latest developments is crucial, such as the European Union has introducing key enhancements related to EU Taxonomy, EFRAG presenting its work programme for 2024 to the Sustainability Reporting Board and the timings outline for upcoming deliverables and the Accounting Directive had been adjusted to encourage more meticulous sustainability reporting.

Here’s a brief overview of the latest developments:

1. Updates to the EU Taxonomy FAQs

To help companies align their sustainability reporting plans with the EU Taxonomy requirements, the European Commission has released a new, expanded FAQ that covers related questions on the EU Taxonomy Climate Delegated Act. The Act sets criteria for activities contributing to climate change mitigation and adaptation without harming other environmental objectives.

The Commission also released a separate FAQ focusing on the Disclosures Delegated Act under Article 8 of the EU Taxonomy Regulation, specifically related to reporting Taxonomy-eligible and Taxonomy-aligned activities and assets.

Alignment with the existing EU Taxonomy rules is mandated in both the upcoming Corporate Sustainability Reporting Directive (CSRD) as well as the current Sustainable Finance Disclosures Regulation (SFDR). Hence, any enhancements to the EU Taxonomy are intended to support these relevant regulations, and the latest FAQs aim to pre-empt any questions and/or confusion as CSRD takes effect.

2. Launch of Key European Sustainability Reporting Work Programmes for 2024

The European Financial Reporting Advisory Group (EFRAG) presented its work programme for 2024 to the Sustainability Reporting Board, outlining the timings for upcoming deliverables. EFRAG serves as the technical adviser to the European Commission and its task is to develop the draft European Sustainability Reporting Standards (ESRS) that will be used by all companies subject to the CSRD.

EFRAG’s Sustainability Reporting 2024 Work Programme includes updates on several key initiatives. These include:

Implementation guidance on Value Chain and Materiality Assessment: Approved draft versions of the guidance are due before the end of 2023, and will be followed by a 30-day public feedback period. Final versions are expected to be delivered by January 2024.

Updates on ESRS for listed SMEs (LSME) and Voluntary ESRS for non-listed SMEs (VSME): An Exposure Draft is expected to be published in January 2024 and will be open for a 4-month public consultation. Technical advice related to the standards for SMEs is expected to be submitted to the Commission in November 2024.

Updates on Digital Sustainability Reporting Taxonomy: EFRAG is expected to disclose a draft XBRL (eXtensible Business Reporting Language) taxonomy for ESRS in Q1 2024, which will be subject to a 60-day consultation. XBRL is the open international standard for digital business reporting and is used to deliver human-readable financial statements in a machine-readable, structured data format. The European Single Electronic Format (ESEF) will be used, which is based on Inline XBRL. It is intended to allow users (e.g. analysts and investors), to easily identify individual disclosures and extract numerical data points for analytical purposes. The final guidelines on the publishing rules of ESRS, complementing the creation of a European Single Access Point (ESAP) under the ESEF Regulation, are anticipated to be issued in the latter half of 2024.

Updates on ESRS for non-EU groups: The Commission has extended the deadline for ESRS for non-EU Groups to June 2026. This applies to EU branches or subsidiaries of non-EU companies that generate over €150 million in the EU. The CSRD foresees the adoption of separate standards that will apply especially for cases of such non-EU companies. An Exposure Draft of these standards is expected to be issued for public consultation by Q4 2024 or Q1 2025.

Updates on sector-specific ESRS: The Commission has extended the deadline for sector-specific ESRS to June 2026. EFRAG is prioritising the development of certain standards, including a general approach to sector ESRS, sector-classification ESRS, and standards for two high-impact sectors, possibly Oil & Gas and Mining, with two additional sector standards expected in the first half of 2024.

Updates on financial sector ESRS: The Nominations Committee is currently in the process of selecting members for the Advisory Panel on financial sector ESRS. The standard-setting research process is expected to start before the end of 2023, with drafting to begin in the second half of 2024.

The proposal to amend the adoption date of sector-specific and third-country standards will go through a similar review process in the EU Council and Parliament, with the changes expected to come into effect in 2026.

The first set of twelve sector-agnostic ESRS, providing for proportionate but comprehensive reporting of environmental, social and governance matters, is now integrated in the European legal framework. This is a further milestone towards implementing a robust sustainability reporting framework in the European Union.

In addition, EFRAG has launched a Q&A platform to support reporting companies with the implementation of the ESRS. This platform will act as a centralised mechanism to address questions and provide feedback on technical issues from stakeholders. EFRAG will make he questions submitted and the answers provided public (all questions will be anonymised beforehand).

Separately, the European Commission published its 2024 Work Programme and Annexes, which include 18 policy initiatives and 26 proposals and initiatives to rationalise reporting requirements for businesses. The Commission has also submitted 15 proposals to support the rationalisation of reporting requirements adopted since March 2023 and 16 evaluation and fitness checks, indicating a comprehensive approach to streamline and evaluate policies, which can have implications for sustainability and efficiency.

Key developments included in the Work Programme, with potential implications for the 2024 sustainability agenda, include:

The Commission mentioned proposals that need to be finalised in the context of the circular economy, including the ecodesign requirements for sustainable products (ESPR).

The Commission expressed a commitment to reduce administrative burdens by 25%, which included measures like postponing the deadline for adoption of the European Sustainability Reporting Standards.

The Commission expressed its intention to establish a 2040 climate target, with the goal of keeping the EU on track towards climate neutrality by 2050.

The text mentions the adoption of the Digital Markets Act (DMA) and the Digital Services Act (DSA) as part of digital policy, which may have sustainability-related implications related to fair competition and data protection measures.

The Commission’s announcement about opening European supercomputer capacity to ethical and responsible artificial intelligence start-ups indicates a sustainable approach to AI development.

The upcoming Cyber Resilience Act and Cyber Solidarity Act proposals will play a big role in reinforcing cybersecurity, which is crucial for ensuring the sustainability of digital systems.

The Commission’s focus on tax and customs, including the reform of the EU Customs Union, may involve measures related to environmental taxation and trade practices.

The proposal to revise the payment services directive II (PSDII) and establish the legal framework for a digital euro may have implications related to digital financial transactions, including efforts to reduce the carbon footprint of financial processes.

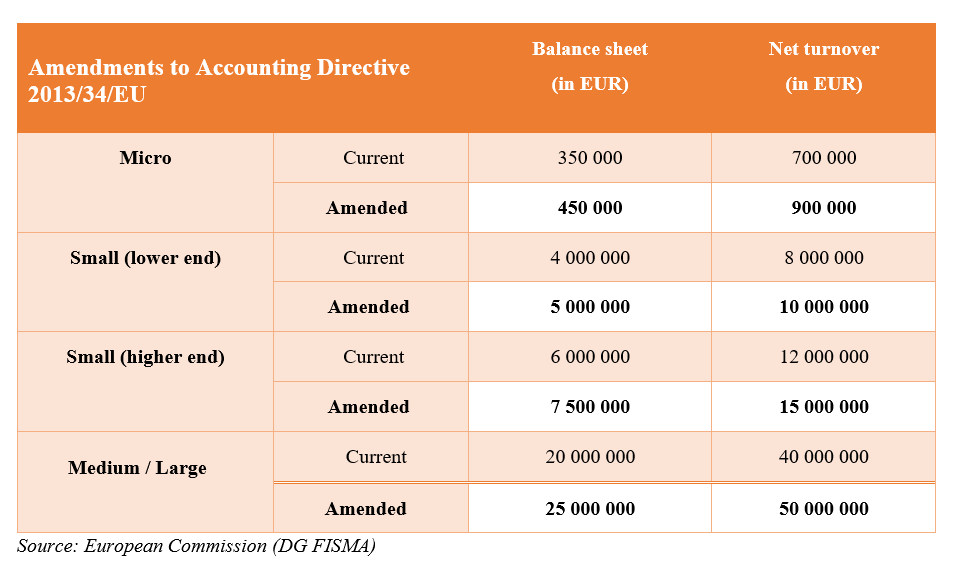

3. Adjustment to Accounting Directive for Inflation – Implications for Sustainability Reporting

The Accounting Directive, first published in 2013 forms the legal basis for single company and consolidated accounts within the European Union (EU). It establishes thresholds for defining companies as micro, small, medium, or large, with implications for accounting as well as sustainability reporting requirements.

In response to mounting inflation in the euro area, the Commission has proposed a notable adjustment to the Directive, suggesting a 25% increase in the size criteria for companies to counteract inflation. This will impact which companies are subject to certain financial and sustainability reporting requirements under the Accounting Directive and the EU Taxonomy Regulation, by essentially increasing the threshold of eligibility.

The changes are taking effect from January 1, 2024. However, these proposed amendments to the Accounting Directive require review by the Parliament and Council. If no objections arise, they will be formally published and implemented three days after the review process, starting from January 1, 2024.

This adjustment to the Accounting Directive underscores the European Commission’s dedication to adapting regulations amid an evolving economic landscape, ensuring that reporting requirements remain effective and efficient. Given these impending changes in sustainability standards, companies should consider conducting assessments to comprehend potential impacts and initiate preparations accordingly.

Conclusion

In conclusion, the recent EU sustainability developments are significant and have far-reaching implications for businesses when it comes to EU sustainability regulations. Understanding ‘What, How, Who and When’ is essential to ensure compliance and leverage the opportunities that these changes present. Companies should proactively assess the potential impacts of these updates for their businesses and prepare for the transition to the new standards. The European Commission’s Work Programme for 2024 emphasises streamlining reporting requirements to reduce administrative burdens and ensure a smooth transition for companies. These cumulative efforts will contribute to a more sustainable and efficient reporting landscape. The CSRD is still set to come into effect in 2024 as part of the EU sustainability regulations, with few delayed rules taking effect at a later date.

Stay tuned for more updates on EU sustainability regulations over the coming months.

If you’re interested in learning more about how GIST Impact can support your company’s CSRD-aligned double materiality assessment, get in touch with us at info@gistimpact.com.